GASB 96 Summary

Understanding the GASB 96 accounting standards

What is GASB 96?

GASB 96, covering Subscription-Based Information Technology Arrangements (SBITAs), was released by the Governmental Accounting Standards Board (GASB) in May 2020. It requires government entities to recognize a right-to-use subscription asset and corresponding subscription liability for such contracts with a specified term. To the extent relevant, the standards for SBITAs are based on the standards established in Statement No. 87, Leases, as amended.

Why the GASB 96 standard was introduced

As cloud-based data management, storage and computing have grown, more organizations are using subscription-based and time-bound IT contracts known as SBITAs, which have similar traits to traditional leases.

Handbook

Preparing for accounting under GASB 96

Looking for help with GASB 96 requirements? Our easy-to-follow handbook is tailored to give you a comprehensive overview of GASB 96 and how to be compliant.

When is GASB 96 effective?

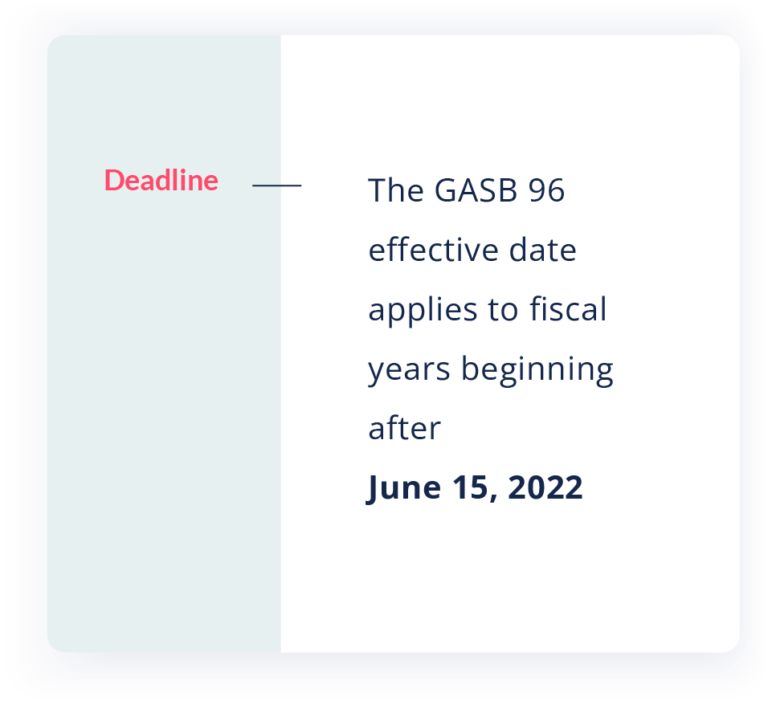

The GASB 96 effective date applies to fiscal years beginning after June 15, 2022, and all reporting years thereafter. The principle is applicable to every state and government entity that enters into an SBITA.

The changes should be applied retroactively by restating financial statements, if practicable, for all prior fiscal years presented. If restatement is not practicable, the cumulative effect, if any, should be reported as a restatement of beginning net position for the earliest fiscal year restated. Assets and liabilities should be recognized and measured using the facts and circumstances at the beginning of the fiscal year in which the standard is implemented.

What’s new for SBITAs?

Prior to GASB 96, there was no specific accounting guidance for SBITAs. GASB 96 provides guidance for the following areas:

- Defines a SBITA

- Establishes that a SBITA results in a right-to-use subscription asset (an intangible asset) and a corresponding subscription liability

- Provides the capitalization criteria for outlays other than subscription payments, including implementation costs of a SBITA

- Disclosures required for SBITA

Key concepts covered under GASB 96

A SBITA is defined as contract that conveys control of the right of use of IT software (belonging to SBITA vendors) for a term and consideration as specified in the contract.

The subscription term is the period during which the government has a non-cancellable right to use the underlying asset. The term also includes option to extend the contract (If it is reasonably certain that the option will be exercised) or option to terminate the contract (if it is reasonably certain that the option will not be exercised).

Subscription liability is initially measured as at the present value of subscription payments expected to be made during the subscription term. Future subscription payments should be discounted using implicit rate (if the implicit rate is determinable) or the government’s incremental borrowing rate.. The government should amortize the discount on subscription liability (for example, interest expense) in subsequent financial reporting periods.

The subscription asset would be recognized and initially measured as:

- The sum of the initial subscription liability amount

- Plus payments made to the SBITA vendor before commencement of the subscription term

- Plus capitalizable implementation costs

- Less any incentives received from the SBITA vendor at or before the commencement of the subscription term. The subscription asset will be amortized over the subscription term.

GASB provides an exception for short term SBITAs, which are 12 months or less, including any options to extend, regardless of their probability of being exercised. Subscription payments for short-term SBITAs would be recognized as outflows of resources over the subscription term.

Setup, payments, modifications, and terminations of SBITAs are essentially identical to leases. Modifications that result in a reduction of the right to use IT assets (specifically including either a reduction in the assets or a shortening of the term) are treated as partial terminations, in which the asset and liability are reduced, and a gain or loss recognized for the difference between the two. This is the same as for GASB 87.

Disclosure requirements under GASB 96

A governmental organization should disclose the following in notes to financial statements about its SBITAs:

- A general description of its SBITAs

- The total amount of subscription assets, and the related accumulated amortization

- Any payments not included in the measurement of subscription

- Variable payments not previously included in the measurement of the subscription liability

- Other payments, such as termination penalties, not previously included in the measurement of the subscription liability

- Principal and interest requirements to maturity for the subscription liability for five subsequent fiscal years and in five-year increments thereafter

- Commitments under SBITAs before the commencement of the subscription term

- The components of any loss associated with an impairment.

GASB 96 examples

We’ve built a set of SBITA accounting examples to help you get started. Use our free GASB 96 SBITA accounting example below to understand how the standard works or see the GASB 96 journal entries in real-time in our free trial.

Use these questions to determine if GASB 96 applies to your contract

Determine if the contract is within the scope of GASB 96 by answering these questions.

Does the contract meet the defnition of SBITA and need to be accounted under GASB 96?

(Note: If you answered Yes then the contract is within the scope of GASB 96 and meets the definition of SBITA)

GASB 96 handbook

Learn about how to adopt the standard and ways to make your implementation successful.

GASB 96 SBITA Accounting Buying Guide

Buying software can be easy if you know the steps to follow.

GASB 96 SBITA Accounting Example

Use this short tutorial to see how to account for SBITAs.

Blog: GASB 96 Summary: Don’t sweat over SBITAs

Get the details on GASB 96 and managing SBITAs.

GASB 96 FAQ

At EZlease.com, we understand the intricacies of GASB standards. While the official GASB 96 implementation guide can be sourced from the Governmental Accounting Standards Board (GASB) website, we also offer comprehensive resources and tools tailored to assist with GASB 96 implementation. Get started with our GASB 96 handbook.