GASB 87 Lessor Lease Accounting Example

Lease accounting examples like this one make it easy to understand the accounting.

Click here to see other lease accounting examples.

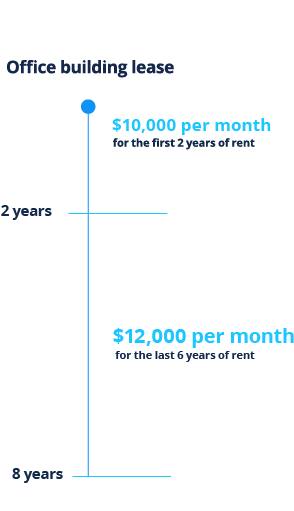

Office building lease example

Let’s take as an example an 8-year office building lease. The first 2 years are at $10,000 per month, and the rent increases to $12,000 per month for the last 6 years. No services are provided to the lessee with the lease.

Additional assumptions: The market value of the building is $1,500,000. These types of buildings typically have an economic life of 50 years. The unguaranteed residual value of the asset is $1,000,000. The lease is initiated and booked on July 1, 2022.

Given the unguaranteed residual value, fair value and the payment stream is known the Implicit Rate will be computed.

Under GASB 87, if you’re the lessor, you need to record a lease receivable and deferred inflow of resources at the start of the lease. The lease receivable is measured as the present value of lease payments expected to be received by the lessor during the lease term. Deferred inflow of resources is measured as the amount of the lease receivable, plus lease payments received from the lessee at or before commencement that relate to future periods, less any lease incentives.

As the lessor, you will need to calculate the amortization of the discount on the lease receivable. Any payments received should be allocated first to the accrued interest receivable and then to the lease receivable. Deferred inflow of resources will be reduced in a systematic and rational manner over the lease term.

Sample journal entries for the first month

[To edit data in the table below, sign up for a free trial of EZLease.]

| Account | Debit | Credit |

|---|---|---|

|

Initial booking |

||

|

Current receivable |

74,750.34 |

|

|

Long term receivable |

800,848.07 |

|

|

Deferred inflow of resources |

|

875,598.41 |

|

Finance lease rent payments |

||

|

Cash finance rent payment |

10,000.00 |

|

|

Current receivable |

|

10,000.00 |

|

Reclassification of finance receivable from long-term to current |

||

|

Current receivable |

6,061.50 |

|

|

Long-term receivable |

|

6,061.50 |

|

Interest accrual for first month |

||

|

Accrued interest |

4,256.93 |

|

|

Interest income |

|

4,256.93 |

|

Lease income |

||

|

Deferred inflow of resources |

9,120.82 |

|

|

Lease revenue |

|

9,120.82 |

Sample journal entries for the second month

[To edit data in the table below, sign up for a free trial of EZLease.]

| Account | Debit | Credit |

|---|---|---|

|

Finance lease rent payment(s) |

||

|

Cash finance rent payments |

10,000.00 |

|

|

Current receivable |

|

5,743.07 |

|

Accrued interest |

|

4,256.93 |

|

Reclassification of finance receivable from long-term to current |

||

|

Current receivable |

6,091.32 |

|

|

Long-term receivable |

|

6,091.32 |

|

Interest accrual |

||

|

Accrued interest |

4,228.69 |

|

|

Interest income |

|

4,228.69 |

|

Lease income |

||

|

Deferred inflow of resources |

9,120.81 |

|

|

Lease revenue |

|

9,120.81 |

To enter this lease in EZLease, follow these steps* :

* System settings are 6/30 Year End with a GASB 87 Implementation date of 7/1/2022.

- Enter a Lease Number and/or name for the lease.

- Enter a Begin Date of July 1, 2022.

- Double-click on the Base Term; in the box that appears, enter 96.

- If not already, displayed, click on the Main data tab, in the Rent Steps grid, enter Gross Rent of 10,000.

- Enter 6/30/2024 for Step End.

- Click on the line below where 10,000 was entered and enter 12,000.

- Enter a Current Economic Life of 600.

- Click on the Inception tab.

- Enter Fair Value of Building/Equipment of 1,500,000.

- Enter an Unguaranteed Residual of 1,000,000.

- Click Save Lease. All accounting has been computed. This will result in a Finance lease. Note the implicit rate has been computed.

- Try running some reports and booking a Journal Entry. Please see the video guide on how to run reports for further information.