Vehicle TRAC Lease Example

Lease accounting examples like this one make it easy to understand the accounting.

Click here to see other lease accounting examples.

Many companies lease cars and trucks. This allows them to use late-model vehicles without worrying about disposing of the vehicle a few years down the road. Often auto leases for businesses come with a TRAC (Terminal Rental Adjustment Clause), which specifies that the auto will be sold at the end of the lease. If the auto sells for a lower price than anticipated, the lessee makes up the difference, while, if it sells for more, the excess is paid back to the lessee. This means that the lessor essentially has no risk and is simply providing financing and management of the vehicle.

If a lessee prefers operating leases, some lessors will adjust the TRAC so that 10.1% of the value of the vehicle is at risk (not covered by the guarantee), which keeps the lease’s present value below 90% of the fair value. This is called a “Split TRAC” lease. Under ASC 842, there are fewer incentives to execute Split TRAC leases than there were under ASC 840, as the lease is still on the balance sheet.

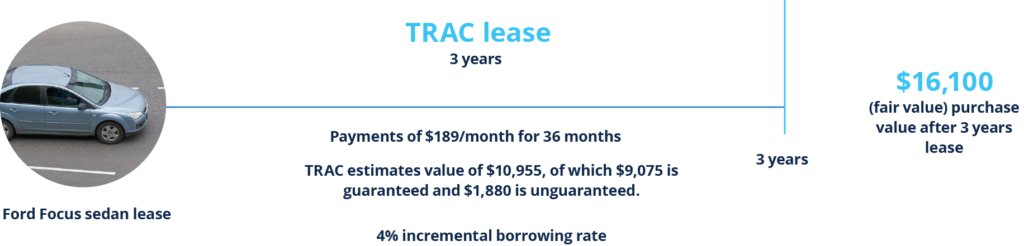

Split TRAC lease

Let’s take an example of a Ford Focus sedan leased for three years using a split TRAC lease, with a commencement date of January 1, 2022. We’ll look at it from the lessee’s side of the transaction. The purchase price (fair value) after rebates would be $16,100. The lease calls for payments of $189/month for 36 months. The TRAC clause stipulates a final estimated value of $10,955, of which $9,075 is guaranteed and $1,880 is unguaranteed. Your incremental borrowing rate (the interest rate you would pay to finance a purchase of the car) is 4%. Let’s assume the Focus has a 7-year economic life.

Under ASC 842

The lease is considered operating and is capitalized at the present value of the rent plus the expected guaranteed residual payment. If it is expected, at the inception of the lease, that the car will sell for at least the $10,955 estimated value, then only the rent is used for capitalization. If the initial direct costs are unknown, we use the incremental borrowing rate of 4% as the discount rate, and the ROU asset and liability are $6,422.91. Since the payments are flat throughout the lease term and there is no timing difference between the straight-line expense and the payments, the liability and net asset will be the same throughout the life of the lease, amortized using the interest method.

Sample journal entries for the first month

[To edit data in the table below, sign up for a free trial of EZLease.]

| Account | Debit | Credit |

|---|---|---|

|

Initial capitalization |

||

|

Operating right-of-use asset |

6,422.91 |

|

|

Operating current liability |

|

2,056.06 |

|

Operating long-term liability |

|

4,366.85 |

|

Monthly rent payment |

||

|

Operating current liability |

168.22 |

|

|

Operating lease cost |

189.00 |

|

|

Operating accumulated amortization |

|

168.22 |

|

Cash rent payments (operating) |

|

189.00 |

|

Liability reclassification, long-term to current |

||

|

Operating long-term liability |

175.08 |

|

|

Operating current liability |

|

175.08 |

Sample journal entries for the second month

[To edit data in the table below, sign up for a free trial of EZLease.]

| Account | Debit | Credit |

|---|---|---|

|

Operating current liability |

168.78 |

|

|

Operating lease cost |

189.00 |

|

|

Operating accumulated amortization |

|

168.78 |

|

Cash rent payment (operating) |

|

189.00 |

|

Operating long-term liability |

175.65 |

|

|

Operating current liability |

|

175.65 |

Under ASC 842, you have to disclose a maturity analysis of your future lease payments separately from other liabilities.

The following is a schedule by years of minimum future payments on noncancelable leases as of Dec. 31, 2022. So, as of the end of year one, the disclosure would be:

| Account | |

|---|---|

|

Year ending December 31 |

|

|

2023 |

2,268 |

|

2024 |

2,268 |

|

Total lease payments required |

4,536 |

|

Less amount representing interest |

169.15 |

|

Present value of net minimum lease payments |

4,366.85 |

Under IFRS 16

Given that the lease is not a low-value lease and doesn’t qualify as a short-term lease (capitalization exemptions), it must be recognized as a finance lease. The calculated initial ROU asset and liability are the same as for ASC 842. However, during the life of the lease, the asset is amortized on a straight-line basis, while the liability is amortized using the effective interest method, which will cause the remaining liability to be larger than the net ROU asset.

To enter this lease in EZLease, follow these steps* :

System settings are 12/31 Year End with an ASC 842 implementation date of 1/1/2022.

- Click 'Add new lease'.

- Enter a Lease Number or name.

- Enter a Begin Date of January 1, 2022.

- Double-click on the Base Term; enter 36 in the pop-up box.

- If not already displayed, click on the 'Main data' tab and in the Rent Steps grid, enter Gross Rent of 189.

- Enter a Current Economic Life of 84.

- Enter an Incremental Borrowing Rate of 4%.

- Enter Fair Value of Building/Equipment as 16,100.

- Click ‘Additional data' tab.

- Enter a Lessee’s Guaranteed Residual of 9,075.

- Enter an unguaranteed residual of 1,880.

- Click 'Save Lease'. Note that the system automatically classified this as an Operating lease at a discount rate of 4% for FASB. Try running a Journal Entry.